staceyhjy1894

About staceyhjy1894

No Credit Score Examine Loans Online: An Observational Examine

In recent years, the monetary panorama has developed significantly, with the appearance of various lending choices aimed toward individuals with much less-than-perfect credit histories. One such option that has gained popularity is the no credit score test mortgage, significantly those provided on-line. This article explores the traits, implications, and shopper behaviors surrounding no credit verify loans, offering an observational analysis of this monetary product.

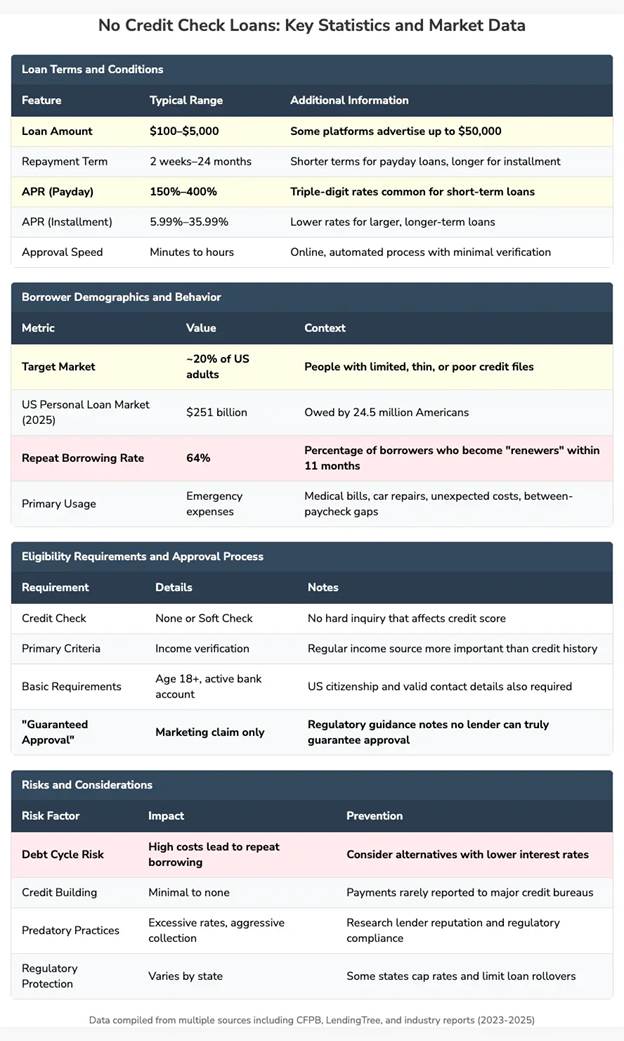

No credit score check loans are designed for borrowers who might not qualify for conventional loans resulting from poor credit score scores or inadequate credit score histories. These loans are sometimes marketed as fast and straightforward solutions for individuals needing fast financial assistance. The method sometimes entails minimal documentation and a fast approval timeframe, making them interesting to those in pressing want of funds.

One among the first traits of no credit score test loans is the pace of the appliance course of. Borrowers can full all the procedure on-line, often within a matter of minutes. This convenience is particularly engaging to individuals going through financial emergencies, resembling medical expenses, automobile repairs, or unexpected payments. Observations indicate that many borrowers are drawn to the immediacy of those loans, usually prioritizing speed over the potential long-term financial penalties.

Additionally, the advertising methods employed by lenders providing no credit score test loans typically emphasize accessibility and ease of use. Commercials steadily highlight the absence of credit checks, which can create a notion of inclusivity. Many consumers, particularly these with poor credit score scores, might feel marginalized by conventional monetary establishments and see no credit score check loans as a viable various. If you have any questions relating to exactly where and how to use fast online payday loans no credit check (bestnocreditcheckloans.com), you can get in touch with us at our own web-site. This notion can lead to an increase in demand, as borrowers perceive these loans as their only possibility for financial relief.

Nonetheless, the implications of obtaining a no credit test loan could be significant. The curiosity rates associated with these loans are often considerably larger than those of conventional loans, reflecting the increased danger that lenders assume when extending credit score to individuals with poor credit score histories. Observational knowledge suggests that many borrowers are unaware of the potential prices related to these loans. As a result, they could find themselves in a cycle of debt, the place they’re compelled to take out further loans to cowl the repayments of earlier ones.

Moreover, the phrases and circumstances of no credit verify loans may be advanced and difficult to know. Many lenders make use of superb print that is probably not adequately defined during the appliance course of. Borrowers might overlook essential details regarding repayment schedules, fees, and penalties, resulting in confusion and financial pressure. Observations point out that a big portion of borrowers specific feelings of frustration and regret after realizing the full extent of their obligations.

Shopper behavior surrounding no credit examine loans additionally reveals a tendency towards impulsivity. Many borrowers report making quick decisions without totally contemplating the consequences. This impulsivity may be attributed to the urgent nature of their financial wants, coupled with the aggressive advertising ways employed by lenders. Observationally, it appears that individuals in distress may not take the time to research alternative choices or search monetary recommendation, typically main them to decide on no credit test loans as a default choice.

Along with the monetary implications, the social stigma surrounding borrowing may also play a job in the decision-making process. Many people with poor credit score histories could really feel embarrassed or ashamed to seek assist from traditional monetary institutions. This stigma can lead to a way of isolation, pushing borrowers in direction of on-line lenders that promise anonymity and discretion. Observationally, plainly the need to avoid judgment can considerably influence the selection to pursue no credit score verify loans, despite the potential dangers concerned.

One other noteworthy side of no credit score verify loans is the demographic profile of borrowers. Observations point out that these loans are notably fashionable among younger shoppers, typically of their late twenties to early thirties. This demographic might lack the financial literacy or expertise to navigate the complexities of borrowing, making them extra vulnerable to the allure of no credit test loans. Additionally, people from decrease-earnings backgrounds are disproportionately represented among borrowers, highlighting a potential socioeconomic divide in entry to financial sources.

In response to the growing popularity of no credit examine loans, regulators and shopper advocacy teams have begun to scrutinize these lending practices. Observational data suggests that there is a rising concern concerning predatory lending practices, as some lenders might exploit susceptible shoppers. Advocacy groups are calling for better transparency and regulation inside the trade to protect borrowers from extreme charges and unsustainable debt cycles.

As the marketplace for no credit check loans continues to expand, it is essential for consumers to train caution and conduct thorough research earlier than committing to any financial product. Observationally, it is clear that many borrowers would profit from increased monetary training and sources to assist them perceive their options. Awareness campaigns aimed at informing shoppers concerning the dangers associated with no credit score test loans might empower individuals to make more informed selections and seek options when potential.

In conclusion, no credit test loans online characterize a complex intersection of convenience, urgency, and danger. Whereas they could present immediate monetary relief to borrowers, the lengthy-term implications may be detrimental if not fastidiously thought of. Observational analysis highlights the need for higher client consciousness and regulatory oversight on this burgeoning market. As the demand for various lending options continues to grow, it is crucial for each borrowers and industry stakeholders to prioritize responsible lending practices and promote financial literacy among consumers.

No listing found.